The boat that is keeping higher education afloat is sinking. College has never been more expensive and never have degrees been so irrelevant in the workplace. The dramatic climb in price for college has led to an enormous amount of student loan debt. According to the Wall Street Journal, students in the graduating class of 2016 were burdened with an average of $37,000 in student loans. Altogether, the number for total student loan debt in the U.S. looms over one and a quarter trillion dollars (Federal Reserve Data). Sadly, those graduates are released into a market with a low demand for college diplomas – the Bureau of Labor Statistics estimates that only 27% of jobs in the United States require a college degree (associates degree or higher). They estimate that by 2022, 50.6 million new jobs will be created, with only 27.1% requiring a four-year degree (Bureau of Labor Statistics). The marketplace is already over-saturated with graduates; currently, we sit with 43% of the population (ages 25-34) with a bachelor’s degrees or higher (Ryan). The long-term effects of too many graduates is controversial, but it isn’t outlandish to claim that it all ends badly. In a previous paper of mine, I made a prediction that within 100 years from now the purpose of college will either change, dissolve, or collapse unless a new hull is used. This paper is about that “new hull” – a possible solution to all the problems listed above for higher education.

Before I get into what this life boat is, I want to ease my reader into the subject with some questions to guide the mood. I don’t think it has been asked, but if it has, I have not found the answers on the internet. My question is: Why, when colleges offer a variety of degrees, are they all priced the same? Why is the cost of an engineering degree the same as an arts degree? We all know that a student pursuing engineering will come out of college making much more money than let’s say, a teacher. So, why is the cost of tuition the same? This subject alone is up for debate – which is my purpose here.

The underlying motivation for the birth of this paper is to prod uncomfortably deep into college’s pudgy sides. There is this idea that has permeated into our culture that says “In order to get a nice paying job, a four-year degree is required”. Because of this thinking, credential inflation has hit hard. As explained by New York Times, “The Master’s as the New Bachelor’s”, a degree is now needed to stay competitive in the workforce and has even become the new requirement on resumes (Pappano). But, does this idea really hold up? Is college really serving its purpose? If College was a person, I would want to ask them, “If you do produce qualified graduates, then why don’t you stand by your words and invest in your students? You literally boast of producing the best! So, why wouldn’t you? Is the investment too ‘high risk’?” This question to College is an attack at its foundation. Think about it: if the numbers held up, and it were sustainable, and profitable, for a college to directly invest in its students, then the only reason that colleges would not pull the trigger is because they really aren’t producing “qualified graduates”. That is to say, it would reveal that the entire purpose for the institution is without legs. This is a big problem. This is where we stand today.

The goal here is to offer a solution that eliminates student loan debt and at the same time create a culture in education that aligned with helping students reach their highest ambitions. A student graduating college should have the skill, knowledge and ability to add value with whomever they work with. That is not asking much. Yet we have articles like Time Magazine’s, “The Real Reason New College Grads Can’t Get Hired” explaining that employer’s biggest complaints are that the new grads can’t think critically and creatively, solve problems or write well (White). I don’t entirely fault College for struggling with this, it’s a problem baked into what has been called “formal education” for 150 years. Well, time to wake up, its 2017. Technology is developing at incredible speeds; as seen in a paper by the Economist, “routine jobs” are becoming automated and the “non-routine”, high skill and low skill jobs, are expanding (Morgenstern). A formal education does not prepare students for any type of skilled work and therefore does not prepare anyone for the new job landscape. The primary drivers of that landscape are college dropouts like Gates and Jobs – neither were inspired by their formal education. While I don’t claim to have the key for inspiration, I do claim to have something to get the ball rolling in that direction.

Introducing a venture capital solution (VCS) –> Let’s pay for college by pledging a percentage of a student’s net worth after graduation.

Here is a visual of the base model:

No, this is not Shark Tank. This is a version of college that is just terribly picky of who they let in.

There are hard numbers for this but I want to address something first.

A thought might be there in the back of your mind: This idea isn’t original. This has been done before, in fact, doesn’t the government offer something similar right now?

This is what the Federal Government offers:

- Income Based Repayment (IBR plan) – Only for borrowers on or after July 1st, 2014

- Revised Pay As You Earn Repayment Plan (REPAYE Plan)

- Pay As You Earn Repayment Plan (PAYE Plan) – Only on or after Oct, 1st 2007

- Income-Contingent Repayment Plan (ICR Plan)

To qualify for any of these, generally your debt needs to exceed your annual salary. Debtors in this scenario are required to pay 10% or more of their total income each year for any of these repayment programs. All of this can be found on the federal student aid website.

Let’s draw a quick compare and contrast here:

| Government Repayment Plans | Similar/Dissimilar | Venture Capital Solution |

| Form of debt | Similar | Form of debt |

| Amount due in repayment has some flexibility. | Not Similar | Amount due in repayment is a fixed rate. (Flat Tax) |

| Doesn’t work without knowledge of income | Similar | Doesn’t work without knowledge of income |

| Only works if student’s monetary wealth is low | Opposite | Only works well if student is monetarily successful |

This is not at all the same as VCS. With VCS, the student does not repay the government for helping pay for school, the student repays the school directly. The school takes the risk. There is no government aide necessary, government is cut out entirely. It’s not a “Graduate Tax”, it’s not some other alternative, it’s a student paying for their education with the capital they create.

Got it. So how does this work? These are the major problems to address:

- How are the costs of educating getting covered while waiting for the return on the investment?

- How are we going to ensure the student repays their debt?

Answering number one gets right down to reimagining the entire purpose for college. Who is going to fund it? There are only two options. We could either have the private market fund it, or government tax dollars fund it.

- Reasoning for private market: If the whole point of college today is to produce a highly qualified workforce, then why not have the employers fund it?

- Reasoning for Government/Tax Dollars: Preserves academic culture that is vital for scholarly work.

Which gets the job done? Unfortunately, those are topics for entire papers by themselves. I am torn myself, but as of now, I lean with the private market solution because it forces an overhaul.

Answering number two is a little trickier. According to the N.Y. Fed, “11.2% of aggregate student loan debt was 90+ days delinquent or in default in 2016” (Federal Reserve Data). Meaning, even with coercion, getting people to pay back their loans is not a small task. Probably, a more invasive method would be created to reduce delinquency. An interesting idea might include the college building bank just for those that sign the contract. There would be a bank-wire tap apart of the contract. To encourage students to use the schools bank, the school might lower their percentage rate so going to a private bank would be costlier. There are many ways to go about less delinquency, and not all can be covered here. The good news is people seem to care less and less each year with just checking all the boxes, “yes, you have my permission to use my information”, as long as its convenient.

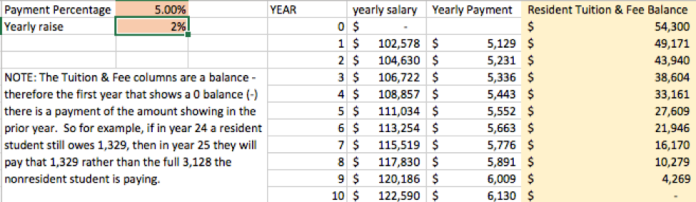

Now for the brass tax. The numbers. VCS model goal is to create a revenue stream with positive net income after 10 years. For this work, students can pledge no less than 1.5% of their net worth (even if they are millionaires or billionaires). But, realistically, it will probably cost somewhere between 4.5-5.5% the students net worth. Here is an image of a little excel spread sheet using real numbers from ASU’s MBA alumni. Spreadsheet courtesy of ASU’s Senior Director of Planning and Budging, Rebecca Barber.

In the graph, we started with the mean salary of an MBA grad at ASU and found that the student would be able to generate revenue after 9 years in repayment. This is a positive example of this program working if it was used alongside what is in place today.

But we want to be more accurate! We want to isolate the numbers to see if it would work by itself. To do this, we are going to scale down to just one department within the college, the Masters in Business Administration program. Here are some real cost factors to consider:

- It costed ASU about $43 million to run the MBA program this past year

- Costs go up each year with demand, inflation must be considered as well

- Costs of students dropping out and not finishing (11.2% delinquency rate)

The goal is to cover costs and create positive net wealth in 10 years or less. So, whether it is realistic or not, we are going to pretend that VCS will entirely replace ASU’s tuition to cover the costs. Here are some things to consider:

- Realistically, costs will go down because the program will shrink. The college isn’t going to take a chance on anyone, the candidate must be high quality. A smaller class size means less resources, and ultimately less everything. Let’s assume two-thirds less for all.

Here are what the numbers look like with all of this in mind:

- The first graduating class produces $705,224 at 5.5% from their income alone.

- Combining both the Economist Intelligence Unit and WorldatWork 2015-2016 Salary Budget Survey, grads should expect a 1.5% salary increase each year ahead of inflation over the next 10 years.

- Also, we are figuring American net worth, not just salary. According to the Federal Reserve, household net worth is stocks, bonds, homes and other assets, minus mortgages and other debts. The average net wealth of an American is $182k (Dogen)

I don’t want to overwhelm my reader so I wont include everything. (There are at least a dozen more factors to consider adding to the equation) So here is a brief, “Final Synthesis”: At 10 years, ASU would bring in $258,00 in positive net revenue. Success!

- For those that are curious of the math: 1327 grads * $207k *5.3% = $14.56 mil

If you are wondering where I got $207,000 if the average americans net wealth is $182,000, you have to remember that these are MBA grads making much more money than the “average american” and MBA grads are generally more financially literate than the “average american. That said, these numbers are rough. Everything is completely rounded off, averaged and then projected ten years into the future. The main factor I didn’t consider was how high the costs would go up sustaining two addition graduates each year. A lot more work is needed to produce an even more accurate number.

A full realization of this model would solve a big issue: price. Full blown VCS would diversify the price of college degrees. The price for a Med degree then depends on its demand and the amount of risk the college is willing to endure. The cost of a Med student dropping out is far higher than the cost of a teacher. Maybe the Med degree then is worth 6% total net wealth and a teaching degree is worth 3.5%. College would then integrate with the market. Not only that, college becomes a predictor for market’s demand in any job field. For example, if a radiologist technician is replaced by automated machines, the college would then see a small drop in revenue with people graduating with a Radiologic Technology degree. In this case, it would be wise for a percentage (of the percentage) to also fund the specific school that the student graduates from. That way, degree programs would lose funding and crumble while new programs would sprout up with demand. Of course, the serious consequence of this is the potential loss of scholarly study. We might see the loss of Philosophy, History, English, Mathematics, all pillars of formal education. The only colleges that could sustain itself with an outdated curriculum are those that produce valuable work in the field. For this reason, it would be rarely offered on college campuses.

So, what are the chances of a college picking this up and trying it? Probably pretty low and this is why: Risk. I had the privilege of speaking with Dr. Rebecca Barber, Senior Director of Planning and Budgeting at ASU. She explained to me that ASU directs all their excess funds to the student body: “We are a nonprofit, and all monies in excess of expenses are reinvested in support of the mission of the institution”. Ok, so where does ASU get their funds? ASU gets 17% of the state’s budget, about $300 million, to run the college. That amount nowhere near covers ASU’s total costs – it costs over $150 million just to run W.P. Carry’s School of Business (and there are 16+ other major schools to fund). The next largest source of income for ASU are Pell Grants; however, the bulk of cost is covered by general tuition and fees. Dr. Barber says this about the colleges finances, “You can make a good argument that the cost of providing an education is equal to the amount of tuition received by the institution.” She explains that ASU, from a business standpoint, isn’t motivated to “make money”, it’s motivated to make enough money to keep up with the demand. This would explain a disinterest in having any skin in the game, a disinterest of having any risk.

However, there is one college out there that is offering something like VCS, and that college is Purdue. Purdue University offers something called an Income Share Agreement. Purdue has partnered with a group of private investors to create “The Back a Boiler-ISA Fund”. It helps students pay for school with the promise that they will pay it back using a percentage of their income after graduation. It is available only to sophomore, junior and senior level students. They too plan for the student to pay back their loan in 10 years or less. The percentage is determined based on the job attained in the field and for this reason, not all degrees are offered. If you would like to learn more, google “income share agreements Purdue”. The research they have accomplished is exciting. Time will only tell if their program is the beginning of a new dawn in education.

As I have already stated, the purpose of this paper is to get a conversation going. The solution put forward is merely to show that there is another way. Ultimately, VCS is a response to disappointment in my own education. And not just college education, education in public school districts too. The costs of colleges are 6% ahead of inflation and climbing (Schoen). For this reason, a model like VCS might actually work better where the costs are lower, like high school. There are hundreds of ways this idea can be tweaked and redone. Maybe it works best at trade school or a special kind of high school. VCS is not final, it’s a solution towards a more inspiring education – for inspiration comes not from ivory towers but from the raw, natural ambition of those wielding it.

Work Cited

Bureau of Labor Statistics. “EMPLOYMENT PROJECTIONS — 2012-2022.” Bureau of Labor Statistics U.S. Department of Labor (2013): n. pag. Bls.gov. U.S. Department of Labor, 9 Dec. 2013. Web. 4 May 2017. <https://www.bls.gov/news.release/archives/ecopro_12192013.pdf>.

Dogen, Sam. “The Average American Net Worth Is Huge!” Financial Samurai. Financial Samurai, 24 Sept. 2010. Web. 03 May 2017.

Federal Reserve Economic Data. New York: Federal Reserve Bank of New York, 01 February 2017. Internet resource. https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2016Q4.pdf

Mitchell, Josh. “Student Debt Is About to Set Another Record, But the Picture Isn’t All Bad.” The Wall Street Journal. Dow Jones & Company, 02 May 2016. Web. 04 May 2017.

Morgenstern, Michael. “Automation and Anxiety.” The Economist. The Economist Newspaper, 25 June 2016. Web. 03 May 2017.

Pappano, Laura. “The Master’s as the New Bachelor’s.” The New York Times. The New York Times, 23 July 2011. Web. 03 May 2017.

Ryan, Camille L., and Kurt Bauman. “Educational Attainment and Outcomes.” (n.d.): n. pag. Census.gov. United States, 1 Mar. 2016. Web. 4 May 2017. <https://www.census.gov/content/dam/Census/library/publications/2016/demo/p20-578.pdf>.

Schoen, John W. “The Real Reasons a College Degree Costs so Much.” CNBC. CNBC, 08 Dec. 2016. Web. 04 May 2017. <http://www.cnbc.com/2015/06/16/why-college-costs-are-so-high-and-rising.html>.

White, Martha C. “The Real Reason New College Grads Can’t Get Hired.” Time. Time, 10 Nov. 2013. Web. 28 Apr. 2017.

A very well written, thought provoking article. The author Chase Gielda asks questions that deserve a discussion. I hope others get involved in this dialogue.

LikeLike